By Ryan Orsatti, Texas personal injury attorney, Ryan Orsatti Law, San Antonio.

Quick Answer

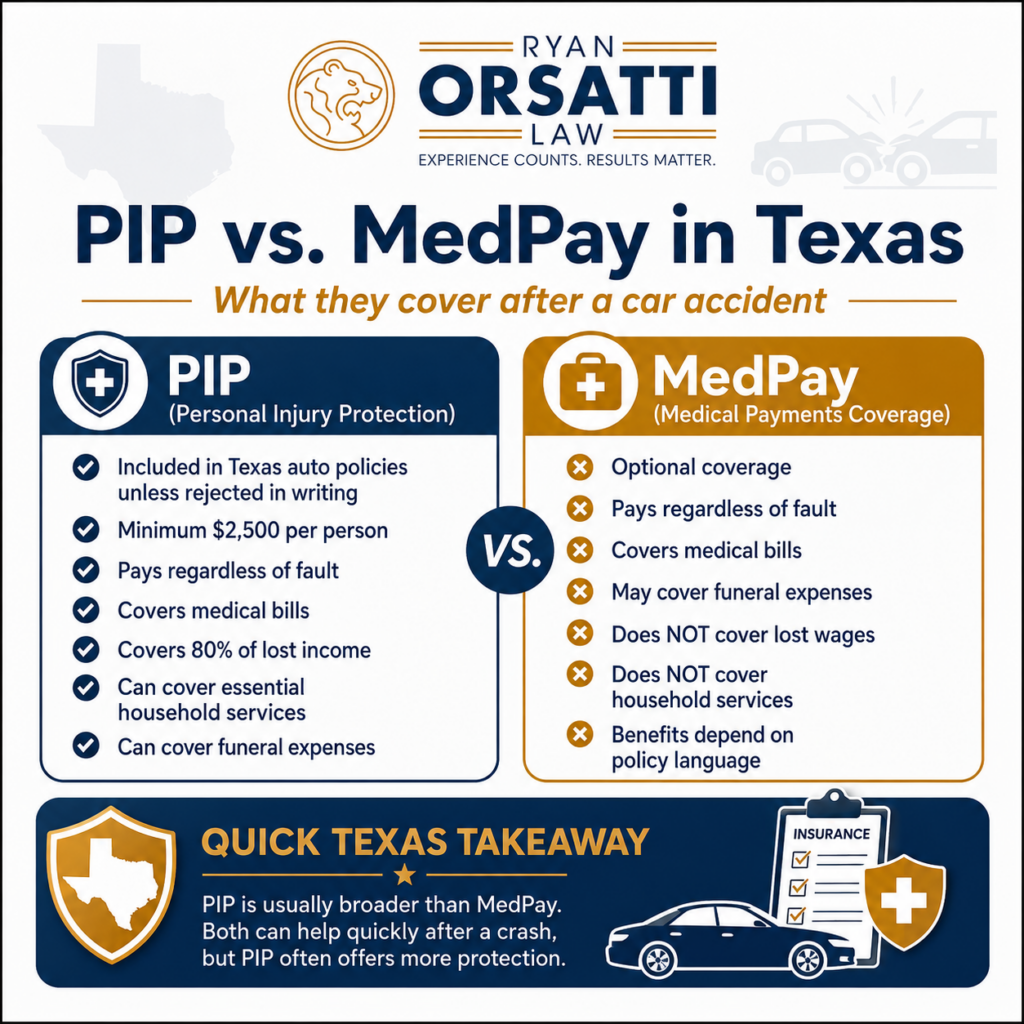

PIP and MedPay in Texas are coverages on your own auto policy that can help pay accident-related bills after a car accident, regardless of who caused the crash. Texas insurers must include PIP unless it is rejected in writing, while MedPay is optional and usually narrower. PIP can cover medical bills, funeral expenses, 80% of lost income, and certain household services; MedPay usually covers medical or funeral expenses only. (Office of Public Insurance Counsel)

Key Takeaways

- PIP is broader than MedPay because it can cover medical bills, funeral expenses, lost income, and essential household services.

- Texas PIP must be included unless rejected in writing, with $2,500 per person as the minimum amount insurers must provide if PIP applies.

- MedPay is not required in Texas, and the exact benefits depend heavily on the policy language.

- PIP usually does not have to be repaid from a liability settlement, but MedPay may involve reimbursement or subrogation depending on the policy.

- Using PIP or MedPay does not replace a claim against the at-fault driver for losses beyond those limited benefits.

What Are PIP and MedPay in Texas After a Car Accident?

PIP and MedPay are first-party auto insurance coverages, meaning you make the claim through your own insurance policy after a wreck. Both can pay benefits regardless of fault, which matters because medical bills often arrive before the police report, liability decision, or settlement. The Office of Public Insurance Counsel describes both as coverages that pay regardless of who is at fault. (Office of Public Insurance Counsel)

This is different from a third-party liability claim. A third-party claim is made against the at-fault driver’s insurance company. PIP and MedPay can help with early bills while the liability claim is still being investigated.

In Texas, that can matter quickly. TxDOT’s 2024 county crash report recorded 554,146 total reportable crashes statewide, including 14,905 suspected serious injury crashes and 18,218 suspected serious injuries. (Texas Department of Transportation) For many injured Texans, the first financial pressure is not the final settlement value. It is the ambulance bill, ER bill, missed work, and follow-up care.

Ryan Orsatti Law helps injured people in San Antonio and across Texas review auto insurance coverages, including PIP, MedPay, UM/UIM, liability coverage, health insurance, and medical bill issues after serious crashes.

What Does PIP Cover After a Texas Car Accident?

PIP can cover reasonable accident-related expenses incurred within three years of the crash, including medical care, funeral expenses, lost income, and certain household services. Texas Insurance Code § 1952.151 defines PIP to include reasonable expenses arising from an accident and incurred by the third anniversary of the accident date. (Justia)

PIP may cover:

- Ambulance bills

- Emergency room care

- Hospital charges

- Medical treatment

- Surgery

- X-rays and other diagnostic imaging

- Dental treatment

- Prosthetic devices

- Professional nursing services

- Funeral services

- 80% of lost income

- Certain replacement services for a person who was not earning wages at the time of the crash

The Texas Department of Insurance explains that PIP pays medical bills and also pays for lost wages and other nonmedical costs. TDI also states that all Texas auto policies include PIP unless the insured rejects it in writing. (Texas Department of Insurance)

Who Is Covered by PIP in Texas?

PIP generally covers the named insured, members of the insured’s household, authorized drivers, and passengers or guest occupants of the insured vehicle. Texas Insurance Code § 1952.151 lists those covered categories and ties the benefit to reasonable expenses arising from the accident. (Justia)

That means PIP may help more than just the policyholder. A passenger injured in your vehicle, a family member in your household, or a permitted driver may have access to PIP depending on the policy and facts.

This is one reason the declarations page matters. The declarations page is the summary page showing the policy coverages, limits, vehicles, and named insureds. It is usually the fastest way to see whether PIP or MedPay may apply.

How Much PIP Coverage Is Required in Texas?

Texas insurers must provide $2,500 per person in PIP coverage unless PIP was rejected in writing. OPIC explains that companies must provide $2,500 per person unless rejected in writing, and Texas Insurance Code § 1952.153 states that the required PIP amount does not have to exceed $2,500 per person in the aggregate. (Office of Public Insurance Counsel)

Many Texas drivers buy higher limits, such as $5,000 or $10,000, but the exact amount depends on the policy. After a crash, do not assume you only have minimum PIP. Ask for the declarations page and the full policy.

What Does MedPay Cover in Texas?

MedPay usually covers reasonable accident-related medical or funeral expenses, but it does not cover lost wages or essential household services. OPIC explains that companies are not required to offer MedPay, and MedPay coverage may vary by policy, including time limits or restrictions on what expenses it reimburses. (Office of Public Insurance Counsel)

TDI describes MedPay as coverage that pays medical bills for you and your passengers and may also apply if you are hurt while riding in someone else’s car or while walking or biking. (Texas Department of Insurance)

MedPay can still be useful. It may help cover deductibles, copays, ambulance charges, imaging, or early treatment. But compared with PIP, it is usually more limited because it does not replace income or help with household services.

PIP vs. MedPay in Texas: What Is the Difference?

The main difference between PIP and MedPay in Texas is that PIP is broader and has statutory protections, while MedPay is usually limited to medical or funeral expenses and depends more on policy language. PIP can include lost income and essential services. MedPay generally does not. (Office of Public Insurance Counsel)

| Issue | PIP in Texas | MedPay in Texas |

|---|---|---|

| Must it be included? | Yes, unless rejected in writing | No, companies are not required to offer it |

| Minimum required amount | $2,500 per person if PIP applies | No Texas statutory minimum like PIP |

| Pays medical bills | Yes | Yes |

| Pays funeral expenses | Yes | Usually yes, depending on policy |

| Pays lost wages | Yes, generally 80% of lost income | No |

| Pays essential household services | Yes, in qualifying situations | No |

| Requires proving fault | No | No |

| Repayment risk | Usually strong anti-subrogation protection, subject to statutory exceptions | May involve reimbursement or subrogation depending on policy |

Key takeaway: If you have both PIP and MedPay, PIP is usually the stronger first coverage to review because it covers more categories and has better Texas statutory protections.

Subrogation means an insurer claims a right to be paid back from money you recover from someone else. Texas PIP has important anti-subrogation protection under Texas Insurance Code § 1952.155, although there are exceptions, including situations involving an uninsured driver who lacked required financial responsibility. (FindLaw)

How Do You Use PIP or MedPay After a Car Accident in San Antonio?

You use PIP or MedPay by opening a first-party claim with your own auto insurer and submitting proof that the expenses or lost income are related to the crash. For PIP, Texas law requires payment as claims arise, but no later than 30 days after the insurer receives satisfactory proof of the claim. (FindLaw)

Here is a practical checklist:

- Request your declarations page and full policy. Confirm whether PIP, MedPay, UM/UIM, collision, and rental coverage exist.

- Ask for the written PIP rejection if the adjuster says you have no PIP. In Texas, PIP must be rejected in writing.

- Open a PIP or MedPay claim with your own insurer. This is separate from the at-fault driver’s liability claim.

- Send accident-related medical bills and records. Use itemized bills when possible.

- Send lost wage proof for PIP. Use pay stubs, an employer letter, time missed from work, and medical proof tying the missed work to the crash.

- Track every payment. Save checks, explanations of benefits, ledgers, and provider balance statements.

- Coordinate with health insurance. PIP, MedPay, health insurance, hospital liens, and subrogation claims can affect the net recovery.

- Do not sign a broad release by mistake. A PIP or MedPay claim should not accidentally release the at-fault driver’s liability claim.

If your wreck happened on Loop 1604, I-10, I-35, US-281, Loop 410, or another San Antonio roadway, keep the same documents you would keep for the liability case: crash report, photos, medical records, wage proof, repair estimate, and all insurance letters.

Attorney Insight: Adjusters often ask for “proof” in a way that sounds routine, but missing documentation can delay or reduce payment. The most common PIP problems are incomplete wage proof, bills without matching medical records, unclear treatment dates, and people assuming they rejected PIP without asking the insurer to produce the signed rejection.

Should You Use PIP, MedPay, or Health Insurance First?

You should usually identify every available coverage first, then decide the payment order based on your policy, medical provider billing rules, and reimbursement risk. PIP may be especially useful early because it pays regardless of fault and can cover categories health insurance does not, including lost income. (Office of Public Insurance Counsel)

Health insurance often matters after PIP or MedPay limits are exhausted. But health insurance can also bring subrogation issues, ERISA plan claims, deductibles, copays, and network restrictions. ERISA plans are employer-sponsored benefit plans that may have federal reimbursement rights depending on plan language.

A hospital lien is a legal claim a hospital may assert against part of a personal injury recovery. A lien is different from a regular bill. If hospital lien, health insurance, PIP, MedPay, and liability coverage are all in play, get the billing order and repayment claims reviewed before settlement.

Ryan Orsatti Law reviews these issues in Texas car accident claims, including medical bills, policy limits, PIP, MedPay, UM/UIM, health insurance subrogation, and treatment documentation. Learn more about the firm’s work as a San Antonio car accident lawyer and its guide to Texas car insurance requirements.

Does Using PIP or MedPay Hurt Your Claim Against the At-Fault Driver?

Using PIP or MedPay does not automatically hurt your claim against the at-fault driver. These are separate first-party benefits, and they do not prove you were at fault. PIP benefits are payable without regard to fault, and they can help while the third-party liability claim is still pending. (Justia)

The bigger risk is documentation. If the medical bills submitted to PIP are incomplete, if treatment gaps are unexplained, or if the lost wage proof is weak, the at-fault driver’s insurer may later use those same gaps to argue the injury claim is worth less.

Comparative responsibility means Texas can reduce a person’s recovery by that person’s percentage of fault. If the injured person is more than 50% responsible, Texas law can bar recovery from the other party. PIP and MedPay do not decide that issue, but your statements and documents can still affect the liability claim.

How Long Do You Have to File a Car Accident Claim in Texas?

In most Texas car accident injury cases, the deadline to file a lawsuit is two years from the date the claim accrues. Texas Civil Practice and Remedies Code § 16.003 is the main personal injury limitations statute, and using PIP or MedPay does not extend the deadline against the at-fault driver. (Texas Statutes)

Do not confuse the PIP claim process with the lawsuit deadline. PIP may involve policy proof deadlines and a 30-day payment rule after satisfactory proof, while the injury claim against the at-fault driver has its own limitation period. Government vehicle crashes, minors, wrongful death, and other special situations may involve different rules.

If UM/UIM coverage is involved because the other driver had no insurance or too little insurance, the strategy changes. Ryan Orsatti Law also handles San Antonio uninsured and underinsured motorist claims.

When Should You Talk to a Texas Personal Injury Lawyer About PIP or MedPay?

You should talk to a Texas personal injury lawyer when medical bills, wage loss, coverage denials, liens, UM/UIM, or settlement discussions become unclear. PIP and MedPay may look simple, but they often intersect with liability coverage, health insurance, hospital liens, and subrogation claims.

Legal help is especially useful when:

- The insurer says you rejected PIP but has not provided the written rejection.

- The PIP or MedPay check does not match the bills submitted.

- You are missing work and need wage-loss documentation.

- The at-fault driver has minimum limits or no insurance.

- A hospital, health insurer, or MedPay carrier claims reimbursement.

- The adjuster asks for a recorded statement before you understand the claim.

Ryan Orsatti Law helps injured people in San Antonio, Bexar County, and across Texas evaluate fault, insurance coverage, medical bills, and claim documentation after car accidents. You can also contact the firm through the Ryan Orsatti Law contact page.

FAQ

Is PIP required in Texas?

PIP is included in Texas auto policies unless rejected in writing, but Texas drivers can reject it. OPIC explains that companies must provide $2,500 per person in PIP coverage unless it is rejected in writing. If an adjuster says you do not have PIP, ask for the declarations page and the signed rejection form. (Office of Public Insurance Counsel)

Is MedPay required in Texas?

MedPay is not required in Texas, and insurance companies are not required to offer it. OPIC explains that MedPay can cover reasonable accident-related medical or funeral expenses, but the details may vary by policy. Some MedPay policies have shorter time limits or narrower reimbursement rules than PIP. (Office of Public Insurance Counsel)

Does PIP cover lost wages after a Texas car accident?

Yes, Texas PIP can cover lost income for an income producer, and OPIC explains that PIP pays 80% of lost wages. The insurer may require reasonable medical proof that the injury caused the income loss. Keep pay stubs, employer verification, missed-work dates, and medical notes tying the work restriction to the crash. (Office of Public Insurance Counsel)

Do I have to pay back PIP from my settlement in Texas?

Usually, PIP has strong protection against reimbursement or subrogation in Texas, but there are statutory exceptions. Texas Insurance Code § 1952.155 generally prevents the PIP insurer from recovering benefits from another person or insurer because of the other person’s fault, except in specific uninsured-driver situations. (FindLaw)

Can I use PIP if I caused the crash?

Yes, PIP benefits are payable without regard to fault. That means PIP can apply even if you caused or partly caused the collision, assuming the coverage exists and the claimed expenses qualify under the policy and Texas law. This is different from a liability claim against another driver. (Justia)

Can passengers use PIP after a Texas crash?

Yes, passengers or guest occupants may be covered by PIP under the vehicle’s policy if the policy has PIP and the claim meets the coverage requirements. Texas Insurance Code § 1952.151 includes passengers and guest occupants of the named insured’s motor vehicle among covered persons. Passenger claims can involve special offset issues, so policy review matters. (Justia)

Does PIP or MedPay cover pain and suffering?

No, PIP and MedPay generally do not pay pain and suffering. They are limited insurance benefits for defined economic losses, such as medical bills, funeral expenses, lost income, or essential services depending on the coverage. Pain and suffering is usually part of the liability claim against the at-fault driver or a UM/UIM claim.

Ryan Orsatti Law

4634 De Zavala Rd, San Antonio, TX 78249

Phone: 210-525-1200

ryanorsattilaw.com

This blog is for informational purposes only, not legal advice. Reading it does not create an attorney-client relationship. Past results do not guarantee future results.

Hurt in an accident in San Antonio? Learn how a San Antonio car accident lawyer can help with your claim. Call 210-525-1200 or request a free consultation. There is no fee unless we win.