Quick Answer

If you’ve been injured in a car accident in Texas, the insurance adjuster assigned to your claim is not on your side—even if they seem friendly and helpful. Adjusters are trained professionals whose job is to close your claim for as little money as possible. That’s not cynicism; it’s how the insurance business model works.

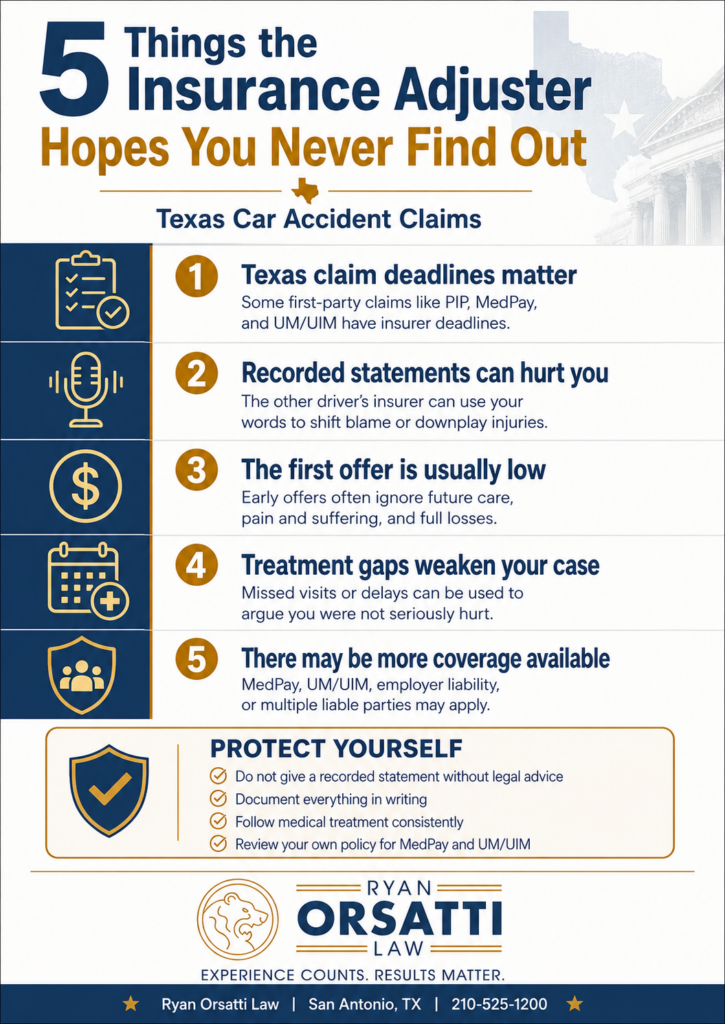

Here are five things the adjuster is counting on you not knowing: Texas law imposes obligations on how insurers handle claims, your recorded statement can be used to reduce your payout, the first offer is almost always a lowball, they know your medical treatment gaps will hurt you, and your claim may be worth far more than what they put on the table. Understanding these tactics can mean the difference between settling for a fraction of what you deserve and recovering full compensation.

1. Texas Law Imposes Deadlines on Many Insurance Claims—But Not Usually on the Other Driver’s Liability Carrier

Most people have no idea that Texas has a law specifically designed to hold insurance companies accountable when they drag their feet on covered claims. It’s called the Texas Prompt Payment of Claims Act, codified in Chapter 542, Subchapter B, of the Texas Insurance Code.

Here’s the important distinction most claimants miss: the Prompt Payment Act applies primarily to first-party insurance claims—meaning claims you file under your own policy (such as MedPay, UM/UIM, collision, or comprehensive coverage). If you’re pursuing a bodily-injury claim against the other driver’s insurance company, those specific statutory deadlines generally do not apply in the same way. The other driver’s insurer still must attempt to handle your claim fairly, but you should not assume Chapter 542 gives you the same deadline leverage that exists on a claim under your own policy.

For many first-party Texas insurance claims, insurers generally must:

| Requirement | Timeframe | Statute |

|---|---|---|

| Acknowledge receipt and begin investigation | Within 15 days after notice of claim | Tex. Ins. Code § 542.055 |

| Accept or reject the claim (one 45-day extension allowed) | Within 15 business days after receiving requested items | Tex. Ins. Code § 542.056 |

| Issue payment after notifying claimant the claim will be paid | Within 5 business days | Tex. Ins. Code § 542.057 |

| Pay the claim if no other statute specifies a deadline | Within 60 days after receiving all requested items | Tex. Ins. Code § 542.058 |

Why does this matter in an injury claim? Because many accident victims also have first-party claims on their own policies—MedPay, UM/UIM, or PIP—and the Prompt Payment Act does apply to those. If your own insurer is stalling on a covered first-party claim, the statutory consequences can include 18% annual interest on the amount owed plus reasonable and necessary attorney’s fees under Texas Insurance Code § 542.060.

Adjusters rarely volunteer this information. They benefit from delay because many claimants get frustrated, give up, or accept a lowball offer just to move on. Understanding the difference between how Texas law treats first-party claims and third-party liability claims helps you know where you have statutory leverage—and where you need other strategies.

What You Should Do

Keep written records of every communication with the adjuster. Even when statutory deadlines are not the main issue, written documentation helps prove when the claim was reported, what information was requested, and how the insurer responded. Follow up phone calls with an email or letter confirming what was discussed.

2. Your Recorded Statement Is a Trap, Not a Formality

Within days of your accident, the adjuster will call and ask you to provide a “recorded statement.” They’ll frame it as routine—just a quick way to get the facts on record. What they won’t tell you is that there is no legal obligation for you to give a recorded statement to the other driver’s insurance company.

Here’s why this matters: adjusters are trained to ask questions designed to create inconsistencies, minimize the severity of your injuries, or establish that you share fault for the accident. Common techniques include:

- Leading with “How are you feeling today?” If you say “fine” or “okay” out of politeness, that answer can later be used to argue your injuries weren’t serious.

- Asking you to describe the accident in detail, then asking again later. Minor differences between your two accounts can be framed as inconsistencies that undermine your credibility.

- Pressing for specifics about your medical history. The adjuster is looking for pre-existing conditions they can use to argue your injuries aren’t related to the crash.

Texas follows a modified comparative fault rule under Chapter 33 of the Texas Civil Practice and Remedies Code. If the insurer can establish that you were 51% or more at fault, you recover nothing. Even partial fault reduces your recovery dollar-for-dollar. Your recorded statement is one of the adjuster’s most powerful tools for building a proportionate-responsibility argument against you.

Attorney Insight

In my practice, I’ve seen adjusters take a claimant’s offhand comment—something like “I didn’t see them until the last second”—and use it to argue the claimant failed to keep a proper lookout. That one sentence, captured in a recorded statement, can shift fault percentages and cost tens of thousands of dollars in reduced compensation. This is why most personal injury attorneys advise clients not to give a recorded statement to the at-fault party’s insurer without legal counsel.

3. The First Settlement Offer Is Almost Never Fair

Insurance adjusters know that people in financial distress—dealing with medical bills, missed work, and vehicle repairs—are more likely to accept a quick payout. That first offer is calibrated to take advantage of urgency, not to reflect the actual value of your claim.

Here’s what the adjuster typically does not account for in an early offer:

- Future medical treatment. If you’re still in treatment or haven’t reached maximum medical improvement (MMI), the full cost of your care is unknown. Accepting a settlement before MMI means you’re guessing at your total medical expenses—and the insurer is betting you’ll guess low.

- Lost earning capacity. Lost wages to date are easy to calculate, but what about the raises, promotions, or overtime you’ll miss if your injury has lasting effects? Early offers rarely factor in long-term economic losses.

- Non-economic damages. Texas law generally allows recovery for physical pain, mental anguish, physical impairment, and disfigurement when supported by the evidence. Quantifying these damages takes time and proper documentation. A rushed settlement almost always undervalues them.

- Future complications. Some injuries—especially soft tissue injuries, concussions, and herniated discs—worsen over time. An early settlement that looks reasonable today may be wildly inadequate six months from now.

Once you sign a release, the case is over. You cannot go back and ask for more money, even if your condition deteriorates or you discover injuries that weren’t apparent at the time of settlement.

Common Mistake

Accepting a settlement offer before you’ve completed medical treatment is one of the most costly mistakes injury victims make. There is no deadline requiring you to accept the insurer’s offer quickly. You have two years from the date of injury to file a lawsuit in Texas under Tex. Civ. Prac. & Rem. Code § 16.003, and the insurer knows this. Use that time wisely.

4. Gaps in Medical Treatment Will Be Used Against You

This is one of the adjuster’s favorite tactics: using gaps in your medical records to argue that your injuries either aren’t serious or weren’t caused by the accident. If you wait weeks between doctor visits, skip physical therapy sessions, or fail to follow up on a referral, the adjuster will point to those gaps as evidence that you weren’t really hurt.

The logic the insurer presents to justify a reduced offer usually looks something like this:

- “If the claimant were truly in pain, they would have sought treatment sooner.”

- “The three-week gap between the ER visit and the follow-up suggests the injury resolved on its own.”

- “The claimant stopped physical therapy after four sessions, which indicates they recovered.”

None of these conclusions may be accurate. People skip appointments for all kinds of legitimate reasons—they can’t get time off work, they lack transportation, they’re uninsured and worried about cost, or they’re simply trying to push through the pain. But insurance adjusters evaluate claims based on documentation, not intent. If it’s not in the medical records, it may as well not have happened.

What You Should Do

- Follow your doctor’s treatment plan consistently, even when you’re feeling better.

- If you need to reschedule, document the reason and reschedule promptly.

- Tell your doctor about every symptom—including ones that seem minor. If you don’t report headaches, sleep problems, anxiety, or radiating pain, those symptoms won’t appear in your records.

- Keep a personal injury journal noting your daily pain levels, limitations on activities, and emotional impact. This type of contemporaneous documentation supports your claim.

5. You May Have Claims You Don’t Even Know About

Most accident victims think of their claim as a single thing: “the other driver hit me, so their insurance should pay.” In reality, there may be multiple sources of recovery that the adjuster has no incentive to tell you about.

Medical Payments Coverage (MedPay). If you have MedPay on your own auto policy, it pays your medical bills regardless of who was at fault—and it doesn’t affect your liability claim against the at-fault driver. Many Texans carry MedPay and don’t realize they can use it immediately to cover treatment costs while their injury claim is still pending.

Uninsured/Underinsured Motorist Coverage (UM/UIM). If the at-fault driver has no insurance or insufficient coverage, your own UM/UIM policy can make up the difference. Texas law requires insurers to offer UM/UIM coverage, and you can only reject it in writing (Tex. Ins. Code § 1952.101). Many policyholders carry this coverage without knowing it.

Multiple Liable Parties. In a commercial vehicle accident, liability may extend beyond the driver to the trucking company, the vehicle owner, a maintenance provider, or even a cargo loader. In a rideshare accident, the driver’s personal policy and the rideshare company’s commercial policy may both apply. The at-fault driver’s adjuster is not going to help you identify other responsible parties.

Employer Liability. If the at-fault driver was working at the time of the crash—making deliveries, driving between job sites, or running errands for their employer—the employer may be vicariously liable under the doctrine of respondeat superior.

Attorney Insight

I regularly see cases where a client’s own insurance policy provides significant additional coverage they didn’t know they had. There may be multiple available coverages—MedPay, UM/UIM, and third-party liability—that apply to the same accident. Identifying and pursuing all of them can substantially increase the total recovery. The at-fault driver’s adjuster will never walk you through this analysis, because it’s not their job to maximize your compensation.

Checklist: Protecting Yourself After a Texas Car Accident

Use this checklist to avoid the most common pitfalls:

- [ ] Do not give a recorded statement to the at-fault driver’s insurance company without consulting an attorney.

- [ ] Document everything in writing. Follow up phone calls with an email summarizing what was discussed.

- [ ] Do not accept the first settlement offer without understanding the full scope of your damages.

- [ ] Follow your medical treatment plan consistently and report all symptoms to your healthcare provider.

- [ ] Review your own insurance policy for MedPay and UM/UIM coverage.

- [ ] Keep a daily injury journal noting pain levels, limitations, and emotional effects.

- [ ] Note every deadline. You have two years from the date of injury to file a lawsuit in Texas (Tex. Civ. Prac. & Rem. Code § 16.003), but evidence and witness memories fade.

- [ ] Consult a personal injury attorney before making any decisions about your claim.

Frequently Asked Questions

Do I have to give a recorded statement to the other driver’s insurance company?

No. You are not legally required to provide a recorded statement to the at-fault party’s insurer. You may have a duty to cooperate with your own insurance company under the terms of your policy, but even then, you have the right to have an attorney present or advise you before doing so.

How long do I have to file a personal injury lawsuit in Texas?

Under Texas Civil Practice and Remedies Code § 16.003, you generally have two years from the date of injury to file suit. For wrongful death claims, the two-year clock begins on the date of the person’s death. Missing this deadline almost always bars your claim entirely, although limited exceptions may apply in cases involving minors, legal incapacity, or other tolling circumstances. Consult an attorney well before the deadline approaches.

What is the Texas Prompt Payment of Claims Act?

It is a set of statutory deadlines in Chapter 542 of the Texas Insurance Code that applies primarily to covered insurance claims under a policy. In many first-party claims—such as MedPay, UM/UIM, or property damage claims on your own policy—insurers must promptly acknowledge, investigate, and pay covered losses. However, those deadlines generally are not the same tool for an injured person making a third-party bodily-injury claim against the at-fault driver’s insurer. An attorney can help you determine which of your claims, if any, are subject to these statutory protections.

Can the insurance company use my social media against me?

Yes. Adjusters routinely monitor claimants’ public social media profiles for photos, check-ins, or posts that could be used to challenge your claimed injuries. A photo of you at a family barbecue can be presented to argue that your injuries aren’t as limiting as you say, regardless of context. Be cautious about what you post while your claim is open.

What if the at-fault driver doesn’t have enough insurance to cover my damages?

This is where your own uninsured/underinsured motorist (UM/UIM) coverage becomes critical. If you carry UM/UIM on your policy, it can cover the gap between the at-fault driver’s limits and your actual damages. Texas law requires your insurer to offer this coverage, and it can only be waived in writing.

Talk to a Texas Personal Injury Attorney About Your Claim

If you’ve been injured in a car accident in San Antonio or anywhere in Texas, don’t navigate the insurance claims process alone. An experienced attorney can identify all available sources of recovery, handle communications with the adjuster, and make sure you don’t leave money on the table.

Ryan Orsatti Law 4634 De Zavala Rd, San Antonio, TX 78249 Phone: 210-525-1200

We offer free consultations and handle personal injury cases on a contingency-fee basis—meaning you pay nothing unless we recover compensation for you.

This blog is for informational purposes only, not legal advice. Reading it does not create an attorney-client relationship. Past results do not guarantee future results.

Hurt in an accident in San Antonio? Learn how a San Antonio car accident lawyer can help with your claim. Call 210-525-1200 or request a free consultation. There is no fee unless we win.