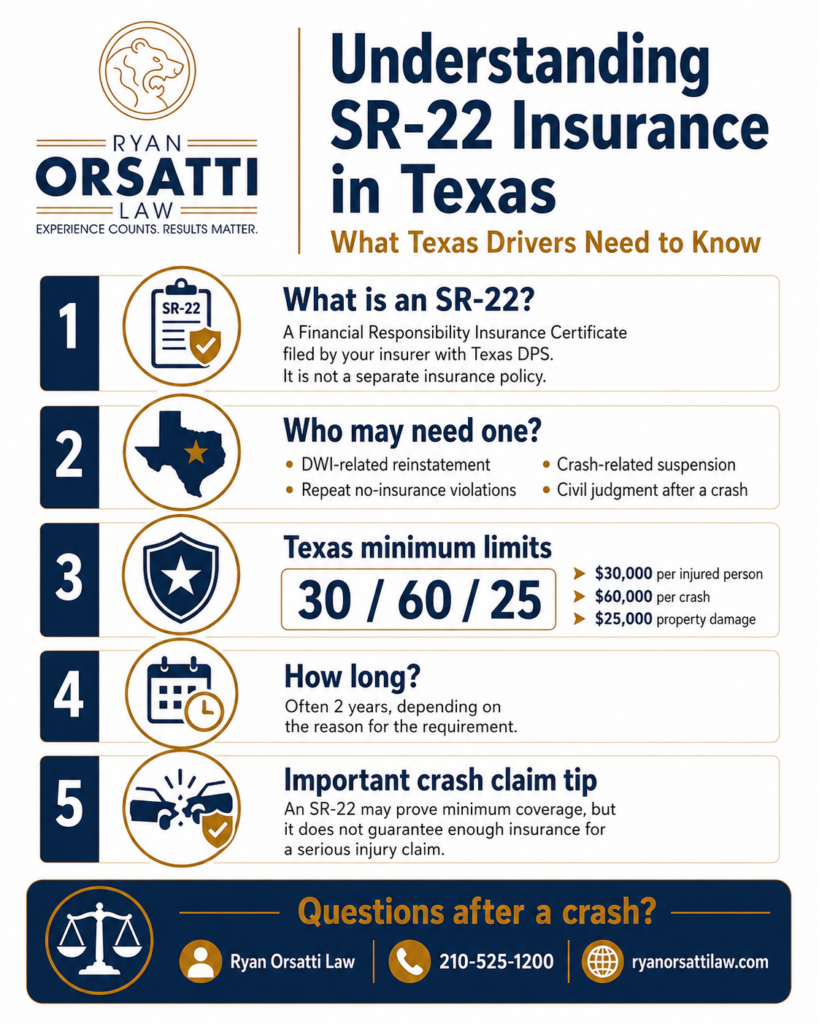

Quick Answer: SR-22 insurance in Texas is not a separate insurance policy. It is a Financial Responsibility Insurance Certificate that your insurer files with the Texas Department of Public Safety to prove you maintain minimum liability coverage under Texas Transportation Code Chapter 601. Texas DPS lists the minimum liability amounts as $30,000 per injured person, $60,000 per crash, and $25,000 for property damage, and many SR-22 requirements last two years from the conviction or judgment date. (Texas Department of Public Safety) If the SR-22 issue involves a crash, injuries, or a coverage dispute, Ryan Orsatti Law can help evaluate the civil injury and insurance issues.

Key Takeaways

- An SR-22 is proof of financial responsibility filed by an insurance company with Texas DPS, not a stand-alone policy. (Texas Department of Public Safety)

- Texas minimum liability coverage is commonly called 30/60/25: $30,000 per person, $60,000 per crash, and $25,000 for property damage. (Texas Department of Insurance)

- DPS says an insurance card or policy will not be accepted in place of an SR-22 when the SR-22 is required. (Texas Department of Public Safety)

- A lapse, cancellation, or termination can trigger another suspension and reinstatement steps. (Texas Department of Public Safety)

- SR-22 coverage does not mean there is enough insurance for a serious injury crash. TDI reported that more than 2.4 million Texas-registered vehicles were not matched to an insurance policy, about 12% of registered vehicles. (Texas Department of Insurance)

- If you were hurt in a crash involving an uninsured, underinsured, or SR-22 driver, review liability coverage, PIP, MedPay, and UM/UIM options before giving a recorded statement or signing a release.

What is SR-22 insurance in Texas?

SR-22 insurance in Texas is a certificate proving that a driver has required motor vehicle liability coverage. Texas DPS calls it a Financial Responsibility Insurance Certificate, and it is filed by an insurance provider with DPS to verify that the driver is maintaining the minimum coverage required by law. (Texas Department of Public Safety)

The confusing part is the name. People call it “SR-22 insurance,” but the SR-22 itself is not what pays a claim. The insurance policy pays covered claims. The SR-22 is the state filing attached to the policy.

For practical purposes, think of SR-22 as a compliance notice. The insurer is telling DPS: “This driver has qualifying liability insurance.” If the policy is canceled, terminated, or lapses, the insurer automatically notifies DPS. (Texas Department of Public Safety)

Who needs an SR-22 in Texas?

A Texas driver may need an SR-22 after certain suspensions, no-insurance violations, crash-related suspensions, DWI-related license issues, or an unsatisfied civil judgment from a crash. DPS specifically says an SR-22 may be required when a driving privilege has been suspended due to a crash, a second or later no-insurance conviction, or a civil judgment. (Texas Department of Public Safety)

Common SR-22 situations include:

- A second or later conviction for no motor vehicle liability insurance

- A crash suspension where financial responsibility must be proven

- A civil judgment arising from a motor vehicle crash

- A DWI conviction where the court or DPS reinstatement process requires SR-22 filing

- An occupational driver license request after certain suspensions

For alcohol-related offenses, Texas DPS says an adult convicted of DWI may be required to obtain an SR-22 from an authorized insurance company and maintain it for two years from the conviction date. (Texas Department of Public Safety) For an occupational driver license, DPS lists an SR-22 as one of the items that must be submitted before the occupational license is issued. (Texas Department of Public Safety)

How much liability coverage does an SR-22 prove in Texas?

An SR-22 proves at least Texas minimum liability coverage, not full protection for every crash loss. Texas DPS and the Texas Department of Insurance both identify the minimum liability limits as $30,000 for bodily injury or death of one person, $60,000 for bodily injury or death of two or more people in one crash, and $25,000 for property damage. (Texas Department of Public Safety)

| Texas SR-22 issue | What it means | Why it matters after a crash |

|---|---|---|

| SR-22 filing | Insurer files proof with DPS | Confirms compliance, not claim value |

| 30/60/25 limits | Minimum liability coverage | Serious medical bills can exceed these limits |

| Insurance card | Not a substitute for SR-22 | DPS requires the certificate when ordered |

| Lapse or cancellation | Insurer notifies DPS | License or registration may be suspended |

| Non-owner SR-22 | Option for drivers without a vehicle | May satisfy DPS filing without insuring a specific car |

Key takeaway: An SR-22 may prove a driver has minimum liability coverage, but it does not prove there is enough insurance to fully cover serious injuries, lost wages, vehicle damage, or long-term care needs.

Does an SR-22 pay for your own injuries?

An SR-22 does not pay for your own injuries. The underlying liability policy generally pays covered damages the insured driver causes to others, while coverages such as Personal Injury Protection, Medical Payments, health insurance, or UM/UIM may help with your own losses depending on the facts and policy language.

TDI explains that liability coverage pays for the other driver’s car repairs and medical expenses when you cause the accident. TDI also explains that PIP can pay medical bills, lost wages, and nonmedical costs, while uninsured/underinsured motorist coverage can pay when the at-fault driver has no insurance or not enough insurance. (Texas Department of Insurance)

For injured people, this matters because a crash claim is not just about whether the other driver had an SR-22. The key questions are fault, policy limits, exclusions, medical proof, lien issues, and whether your own policy includes helpful first-party coverage.

Does an SR-22 mean the driver has enough insurance for a serious crash?

No, an SR-22 does not mean the driver has enough insurance for a serious crash. It usually proves minimum liability coverage, and Texas minimum limits can be too low for multi-vehicle crashes, emergency treatment, surgery, wage loss, or permanent impairment. TDI warns that if a driver does not have enough liability coverage, the driver may have to pay the rest personally and can be sued. (Texas Department of Insurance)

This is why injured Texans should not assume “the driver has insurance” means “the claim is covered.” A policy may have low limits, a named-driver exclusion, a business-use issue, a lapsed SR-22, or other coverage problems.

Ryan Orsatti Law helps injured people in San Antonio and across Texas evaluate insurance coverage after serious crashes, including liability limits, PIP, MedPay, UM/UIM, and medical bill issues.

How long do Texas drivers need to keep an SR-22?

Most Texas SR-22 requirements discussed by DPS last two years from the date of the conviction that triggered the SR-22 or two years from the date a crash-related judgment was rendered. DPS also says failure to maintain a valid SR-22 for the required period can result in additional enforcement actions and reinstatement fees. (Texas Department of Public Safety)

If you file the SR-22 late, DPS does not necessarily restart the two-year period from the filing date. DPS gives an example: if you send in an SR-22 one year after the conviction date, you generally need to maintain it for only one more year, unless a new conviction extends the requirement. (Texas Department of Public Safety)

This timing can matter in real life. A person may believe the SR-22 period is over when the insurer stops billing for the filing, but DPS eligibility is what controls reinstatement status. Check the DPS license eligibility system and keep written proof of compliance.

What happens if SR-22 coverage lapses in Texas?

If required SR-22 coverage lapses, your Texas driving privilege and vehicle registration may be suspended. DPS says suspension can occur if you are required to maintain a valid SR-22 and do not have one on file, or if DPS receives notice that the SR-22 was canceled, terminated, or lapsed and no new SR-22 was filed before cancellation. (Texas Department of Public Safety)

DPS also says that if SR-22 coverage lapses, the driver license or driving privilege may be re-suspended, and a new SR-22 plus a $100 reinstatement fee may be required. (Texas Department of Public Safety)

A lapse can also create insurance problems after a crash. If the policy was not active on the crash date, the injured person may need to examine UM/UIM coverage, other household policies, vehicle-owner coverage, employer coverage, or direct claims against responsible parties.

Can you get an SR-22 in Texas if you do not own a vehicle?

Yes, Texas DPS says a driver who does not own a vehicle should ask an insurance provider about a Texas non-owner SR-22 insurance policy. A non-owner SR-22 is typically used when the person must prove financial responsibility but does not have a specific vehicle to insure. (Texas Department of Public Safety)

A non-owner policy is still liability insurance. It is not a substitute for being properly listed on a household vehicle policy, and it may not cover every borrowed, employer-owned, rideshare, delivery, or business-use situation.

This is a common mistake in San Antonio crash cases. A person may buy a non-owner SR-22 for license compliance, then regularly drive a family member’s car without confirming whether that vehicle’s policy covers them. That can become a coverage dispute after a crash on I-10, Loop 1604, Loop 410, US-281, or I-35.

What should you do if you need an SR-22 after a Texas crash?

If you need an SR-22 after a Texas crash, separate the license issue from the injury and insurance claim issue. DPS compliance is about reinstatement and financial responsibility, while a personal injury claim focuses on fault, medical causation, damages, insurance limits, liens, and deadlines.

Follow this checklist:

- Check your DPS license eligibility status. DPS directs suspended drivers to the license eligibility webpage to determine what must be submitted for reinstatement. (Texas Department of Public Safety)

- Contact an authorized Texas insurance provider. DPS says local agents or providers can issue an SR-22, and non-owner options may be available if you do not own a vehicle. (Texas Department of Public Safety)

- Confirm the filing was actually processed. DPS says SR-22 processing may take up to 21 business days. (Texas Department of Public Safety)

- Pay required reinstatement fees. DPS lists a $100 reinstatement fee for SR-22 reinstatement situations, in addition to other outstanding fees. (Texas Department of Public Safety)

- Do not rely on an insurance card alone. DPS says an insurance card or policy will not be accepted in place of an SR-22. (Texas Department of Public Safety)

- Save crash evidence. Keep the CR-3 crash report, photos, witness names, medical bills, treatment records, repair estimates, wage documents, and all letters from insurers or DPS.

- Review your own coverages. PIP, MedPay, UM/UIM, collision, and health insurance can matter even if someone else caused the crash.

- Talk to the right lawyer for the right issue. A criminal-defense lawyer may be needed for DWI or license consequences. A Texas personal injury lawyer may be needed for injuries, medical bills, fault disputes, UM/UIM, and settlement releases.

Attorney Insight: In injury claims, adjusters do not value a case based on the phrase “SR-22.” They look at coverage, fault evidence, medical documentation, causation, prior injuries, treatment gaps, liens, and policy defenses. An SR-22 may tell us the driver had a filing requirement, but it does not tell us whether the active policy has enough limits or whether another policy may apply.

How does an SR-22 affect an injury claim after a Texas crash?

An SR-22 can affect an injury claim because it signals that insurance compliance may be a central issue, but it does not decide fault or damages. Fault is about how the crash happened, and damages are about the injuries, medical treatment, lost income, pain, impairment, and future care that can be proven.

If the at-fault driver has only minimum liability coverage, an injured person may need to look beyond that policy. UM/UIM coverage is designed for crashes where the at-fault driver has no insurance or not enough insurance, and TDI says insurers must offer UM/UIM when you buy auto insurance unless you reject it in writing. (Texas Department of Insurance)

What should injured people look for after a crash with an SR-22 driver?

Injured people should look for proof of active coverage on the crash date, not just the fact that an SR-22 was once required. The practical documents include the crash report, claim number, insurer name, policy limits disclosure if available, vehicle-owner information, your own declarations page, and any denial or reservation-of-rights letter.

Also watch for these issues:

- The driver may not own the vehicle.

- The vehicle owner may have separate coverage.

- A household exclusion or named-driver exclusion may be raised.

- The driver may have been working, delivering, or using the vehicle for business.

- Minimum limits may not cover all medical bills.

- Your own UM/UIM claim may require notice and cooperation.

- Health insurance subrogation may affect the net recovery.

Subrogation means a health insurer may claim a right to be paid back from a personal injury settlement. A hospital lien is a legal claim a hospital may assert against part of an injury recovery. These issues should be reviewed before signing any release.

For more detail on insurance coverage after a crash, see Ryan Orsatti Law’s guides on Texas UM/UIM coverage, who pays medical bills after a car accident, and PIP coverage in Texas.

Does an SR-22 change the deadline to file a Texas injury lawsuit?

No, an SR-22 does not change the Texas personal injury filing deadline. Texas Civil Practice and Remedies Code § 16.003 generally sets a two-year limitations period for personal injury claims, so the injury claim deadline must be calculated separately from any DPS SR-22 or license reinstatement deadline. (Texas Statutes)

This is a common source of confusion. DPS deadlines affect driving privileges. Insurance claim deadlines and lawsuit deadlines affect civil recovery. A person can be fully compliant with DPS and still miss an injury deadline, or have an active injury claim while still dealing with license reinstatement.

Comparative responsibility means Texas can reduce a person’s recovery by that person’s percentage of fault. In a crash claim, the evidence of how the collision happened matters more than the existence of an SR-22 filing.

When should you talk to a Texas personal injury lawyer about SR-22 issues?

You should talk to a Texas personal injury lawyer when the SR-22 issue is tied to a crash with injuries, disputed fault, low insurance limits, a hit-and-run, UM/UIM coverage, medical bills, or a settlement release. A personal injury lawyer is not a substitute for criminal-defense counsel in a DWI case, but civil injury and insurance issues often run alongside license problems.

Ryan Orsatti Law helps injured people in San Antonio, Bexar County, and across Texas evaluate fault, insurance coverage, medical documentation, and settlement issues after serious motor vehicle accidents. That includes crashes where an SR-22 filing, no-insurance history, or minimum-limits coverage creates practical problems for the injury claim.

For crash-related help, you can review the firm’s San Antonio car accident lawyer page or contact Ryan Orsatti Lawdirectly.

FAQ

Is SR-22 insurance required for every Texas driver?

No. SR-22 filing is not required for every Texas driver. It is usually required after certain license suspensions, crash-related financial responsibility issues, DWI-related reinstatement requirements, second or later no-insurance convictions, or civil judgments from crashes. DPS will identify the requirement through your driver eligibility record or enforcement notice. (Texas Department of Public Safety)

How long does Texas DPS take to process an SR-22?

Texas DPS says SR-22 processing may take up to 21 business days. If your license is suspended, do not assume you are eligible to drive immediately after buying a policy. Check your DPS license eligibility status and confirm all compliance items, fees, and suspension periods have been cleared before driving. (Texas Department of Public Safety)

Can I use my insurance card instead of an SR-22 in Texas?

No. Texas DPS says an insurance card or policy will not be accepted in place of an SR-22 when an SR-22 is required. The SR-22 must be filed by the insurance provider with DPS. Keep your insurance card for traffic stops, but do not treat it as SR-22 compliance. (Texas Department of Public Safety)

What happens if my SR-22 policy is canceled?

If your SR-22 policy is canceled, terminated, or lapses, the insurance provider notifies Texas DPS. DPS says your driving privilege and vehicle registration may be suspended if no new SR-22 is filed before cancellation. A lapse can also require a new SR-22 and a $100 reinstatement fee. (Texas Department of Public Safety)

Can I get an SR-22 if I do not own a car in Texas?

Yes. Texas DPS says drivers who do not own a vehicle should ask an insurance provider about a Texas non-owner SR-22 insurance policy. A non-owner SR-22 may satisfy the filing requirement, but it does not automatically mean you are covered for every vehicle you drive. Always confirm the policy language. (Texas Department of Public Safety)

Does an SR-22 protect me if another driver causes a crash?

No. An SR-22 is tied to the driver who must prove financial responsibility. If another driver causes your crash, your protection usually depends on that driver’s liability coverage and your own coverages, such as PIP, MedPay, collision, and UM/UIM. TDI says UM/UIM can help when the other driver has little or no insurance. (Texas Department of Insurance)

Should I accept a settlement if the at-fault driver has SR-22 insurance?

Do not accept a settlement only because the at-fault driver has SR-22 insurance. First confirm coverage, policy limits, medical bills, future treatment needs, liens, wage loss, and your own UM/UIM options. Once you sign a release, you may give up claims even if later medical problems or coverage issues appear.

Ryan Orsatti Law

4634 De Zavala Rd, San Antonio, TX 78249

Phone: 210-525-1200

ryanorsattilaw.com

This blog is for informational purposes only, not legal advice. Reading it does not create an attorney-client relationship. Past results do not guarantee future results.

Hurt in an accident in San Antonio? Learn how a San Antonio car accident lawyer can help with your claim. Call 210-525-1200 or request a free consultation. There is no fee unless we win.