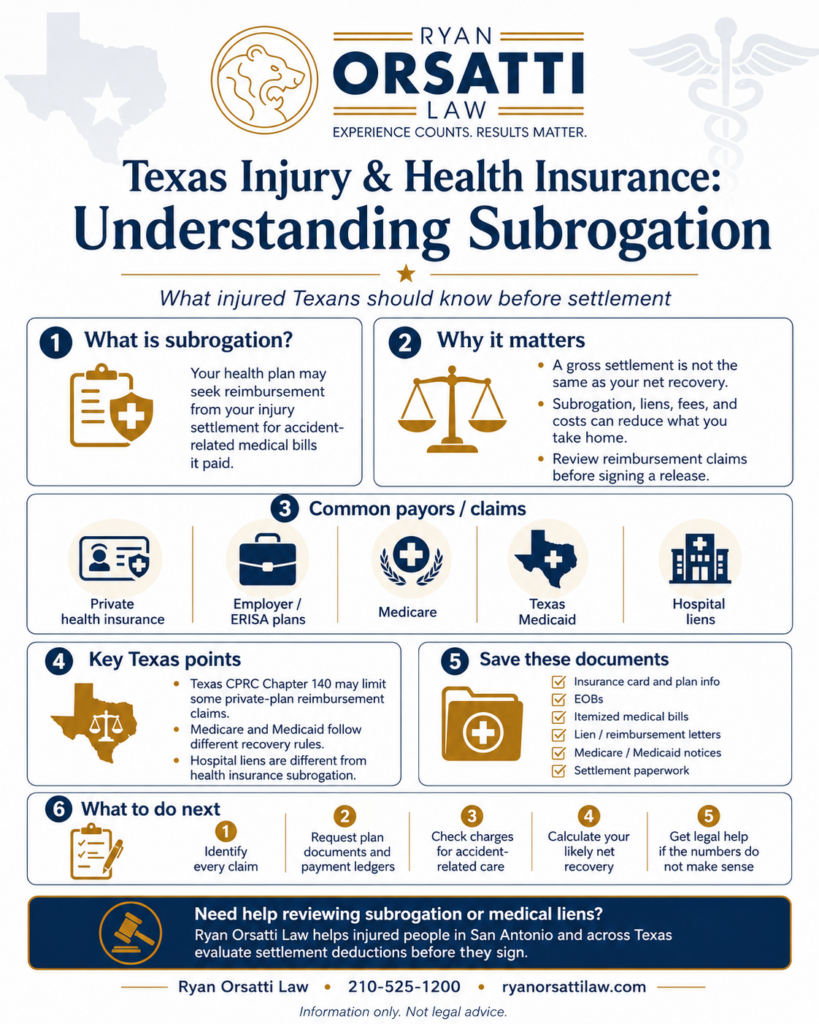

Health insurance subrogation in a Texas personal injury case means your health plan may seek reimbursement from your settlement for accident-related medical bills it paid. In many private health-plan claims, Texas Civil Practice & Remedies Code Chapter 140 limits the payor’s recovery, but Medicare, Medicaid, hospital liens, and some ERISA plans follow different rules. Before signing a release, identify every reimbursement claim, audit the accident-related charges, and calculate your likely net recovery; Ryan Orsatti Law helps injured people in San Antonio and across Texas evaluate these issues before settlement.

Key Takeaways

- Subrogation is a payback claim. If health insurance paid injury-related medical bills, the plan may ask to be repaid from the injury recovery.

- Texas Chapter 140 may limit some private health-plan claims. The cap depends on the gross recovery, attorney fees, procurement costs, and the amount paid by the plan.

- Government benefits are different. Medicare and Texas Medicaid have separate recovery rules that should be handled before funds are disbursed.

- Hospital liens are not the same as health insurance subrogation. Texas Property Code Chapter 55 has its own 72-hour, filing, and lien-amount rules.

- The real settlement number is the net. A gross settlement does not tell you what you actually receive after fees, costs, medical balances, and reimbursement claims.

What Does Health Insurance Subrogation Mean After a Texas Accident?

Health insurance subrogation means the health plan claims a right to be reimbursed if it paid medical bills caused by someone else’s negligence. In plain English, the plan paid first, then says part of the injury settlement should pay it back because the at-fault party or insurer ultimately caused the medical expense.

This issue comes up after car wrecks on Loop 1604, I-10, I-35, Loop 410, US-281, and in other injury claims across Bexar County and Texas. It can also arise in premises liability, commercial vehicle, motorcycle, pedestrian, oilfield, and catastrophic injury cases.

Subrogation is not always called “subrogation” in the paperwork. You may see words like:

- Reimbursement

- Recovery rights

- Third-party liability

- Conditional payments

- Lien

- Right of recovery

- Overpayment recovery

The exact wording matters. A private health insurance plan, a self-funded employer plan, Medicare, Medicaid, a hospital, and a treatment provider may all have different rights.

Why Does Subrogation Matter Before You Settle a Texas Injury Claim?

Subrogation matters because it affects the amount you actually take home from a Texas personal injury settlement. A settlement can look strong on paper, but the net can shrink if health insurance reimbursement, Medicare, Medicaid, hospital liens, provider balances, case expenses, and attorney fees are not calculated before the release is signed.

TxDOT reported that in 2024, Texas had 14,905 serious injury crashes and 18,218 people sustaining serious injuries, with one person injured every 2 minutes and 5 seconds in reportable crashes. Serious injury claims often involve ER visits, imaging, follow-up care, therapy, injections, surgery evaluations, and multiple payors, which makes subrogation review a practical part of settlement planning.

A release usually ends the injury claim against the at-fault party or insurer. If reimbursement claims are not resolved before disbursement, the injured person may still face collection demands, delayed checks, or a dispute over who should receive settlement funds.

For related settlement planning, see Ryan Orsatti Law’s guide on what costs come out of a personal injury settlement besides attorney fees.

Which Texas Rules Control Health Insurance Subrogation?

The rule that controls depends on who paid the medical bills and what kind of plan paid them. Texas Civil Practice & Remedies Code Chapter 140 governs many contractual health-plan subrogation claims, but Medicare, Medicaid, workers’ compensation, hospital liens, and self-funded ERISA plans may require separate analysis.

How Does Texas Civil Practice & Remedies Code Chapter 140 Limit Some Private Health-Plan Claims?

Texas Civil Practice & Remedies Code § 140.005 limits certain payors’ recovery in covered cases by using formulas tied to the injured person’s gross recovery, the benefits paid, attorney fees, and procurement costs. If the injured person is represented by an attorney, the payor’s claim is generally reduced by attorney fees and costs under the statute’s framework.

This matters because a health plan may initially demand full reimbursement even when Texas law limits what it can collect. The demand should be compared against the plan documents, the payment ledger, the settlement amount, the attorney fee, and the costs that helped create the recovery.

The “made whole” doctrine means the idea that an insurer should not recover until the injured person has been fully compensated. For payor recovery governed by Texas Civil Practice & Remedies Code § 140.005, the statute says that common-law made-whole doctrine does not apply.

What Is Different About Medicare, Medicaid, and ERISA Health Plans?

Medicare, Medicaid, and ERISA plans do not work like ordinary private health insurance subrogation claims. CMS says Medicare conditional payments must be repaid when a settlement, judgment, award, or other payment is made, and Texas Medicaid third-party liability rules require recovery from legally responsible third parties when Medicaid paid for covered medical services.

A self-funded private employer health plan can be especially important. The U.S. Department of Labor explains that private-sector employment-based group health plans that self-insure are generally not subject to state health insurance laws. That means a plan that looks like “Blue Cross,” “Aetna,” “UnitedHealthcare,” or “Cigna” on the card may actually be funded by the employer, with the insurer only administering claims.

The practical first step is to request the plan documents, not just the insurance card. In many cases, the Summary Plan Description, plan document, lien letter, and payment ledger decide the next move.

How Are Subrogation, Hospital Liens, and Provider Balances Different?

Subrogation, hospital liens, and provider balances are different types of claims against settlement funds. A health insurer usually claims reimbursement for bills it paid, a hospital lien is a statutory claim under Texas Property Code Chapter 55, and a provider balance is often a contract or unpaid bill issue.

| Claim type | Who asserts it | What it usually covers | Key Texas issue |

|---|---|---|---|

| Health insurance subrogation | Private health insurer, employer plan, or plan administrator | Accident-related medical bills paid by the plan | Chapter 140 may limit some claims, but ERISA and plan language matter |

| Medicare conditional payment | CMS through the Medicare recovery process | Injury-related Medicare payments | Must be reported and resolved before or during settlement handling |

| Texas Medicaid recovery | Texas Medicaid or its recovery contractor | Injury-related Medicaid payments | Medicaid is generally payer of last resort and may seek reimbursement |

| Hospital lien | Hospital or qualifying emergency medical services provider | Emergency and hospital care tied to the accident | Texas Property Code Chapter 55 has 72-hour, filing, and amount rules |

| Letter of protection or provider balance | Doctor, facility, therapist, chiropractor, imaging center, or other provider | Unpaid treatment charges | Usually handled through contract review, bill audit, and negotiation |

Key takeaway: Do not treat every medical deduction as the same type of lien because each category has different rules, defenses, deadlines, and negotiation leverage.

For more background on lien categories, see Ryan Orsatti Law’s guide to medical liens in Texas personal injury settlements.

How Do Texas Hospital Liens Affect Injury Settlements?

Texas hospital liens can attach to a personal injury claim when a hospital provides services for accident injuries attributed to another person’s negligence and the patient is admitted not later than 72 hours after the accident. Texas Property Code Chapter 55 also addresses what the lien attaches to, including certain claims, judgments, and settlement proceeds.

Hospital liens are often confused with health insurance subrogation, but they are not the same thing. A hospital lien is filed by a provider seeking payment for its charges. A subrogation claim is usually asserted by a payor that already paid medical bills.

Texas Property Code § 55.004 limits a hospital lien to the lesser of certain statutory amounts, including the hospital’s charges for services during the first 100 days of hospitalization, 50 percent of the recovery, or the amount awarded for hospital charges if specified by the factfinder, reduced as provided by the statute.

A hospital lien should be checked for:

- Date of accident.

- Date of admission.

- Whether the treatment was accident-related.

- Whether the lien was properly filed.

- Whether the claimed charges are reasonable and regular.

- Whether insurance was available and should have been billed.

- Whether the claimed lien amount exceeds the statutory cap.

If you are dealing with medical bills after a wreck, Ryan Orsatti Law also has a guide on who pays medical bills after a car accident.

Should You Use Health Insurance After an Accident If Subrogation May Apply?

In many Texas injury cases, using health insurance for accident-related treatment can still be the right move, even if subrogation may apply later. Health insurance may reduce billed charges to contracted rates, prevent collections, improve access to care, and create a clearer payment record, but the reimbursement claim must be tracked.

The worst option is usually letting bills pile up without a plan. Texas Civil Practice & Remedies Code Chapter 146 has timely billing rules for health care providers, including billing by the first day of the 11th month after services in many circumstances, and it can bar certain claims if the provider violates the statute.

Health insurance also affects damage proof. Texas Civil Practice & Remedies Code § 41.0105 limits recovery of medical or health care expenses to the amount actually paid or incurred by or on behalf of the claimant. That means the billing history, insurance adjustments, outstanding balances, and provider agreements all matter.

Attorney Insight: In settlement negotiations, the gross number is only half the conversation. A careful lawyer looks at the net worksheet before recommending settlement. That means checking every EOB, lien notice, hospital filing, Medicare or Medicaid letter, and provider balance. A case with a lower gross offer can sometimes produce a better client net than a higher offer with unresolved reimbursement problems.

What Documents Should You Save for a Texas Health Insurance Subrogation Review?

You should save every document that shows who paid, who billed, what was adjusted, and what remains owed. The most useful subrogation file includes health insurance records, provider bills, explanations of benefits, lien letters, Medicare or Medicaid notices, and the final proposed settlement statement.

Use this checklist:

- Health insurance card and policy information. Save the card, group number, plan name, and any employer benefits information.

- Explanation of Benefits documents. EOBs show what was billed, what was allowed, what was paid, and what may remain patient responsibility.

- Itemized medical bills. Get itemized bills, not just balance summaries.

- Subrogation or reimbursement letters. Forward every letter from Optum, Rawlings, Equian, Conduent, Benefit Recovery, CMS, TMHP, or any plan recovery vendor.

- Hospital lien notices. Keep any county clerk filing notice, hospital letter, or EMS lien notice.

- Medicare and Medicaid notices. Medicare conditional payment letters and Medicaid recovery notices should be reviewed for unrelated charges.

- Settlement documents. Keep the release, settlement statement, disbursement sheet, and correspondence about lien reductions.

- Provider contracts or letters of protection. Save any treatment-on-lien agreements you signed.

Key takeaway: The documents that seem like routine insurance paperwork during treatment often become the documents that decide how much money is deducted at settlement.

What If the At-Fault Driver Does Not Have Enough Insurance?

If the at-fault driver does not have enough insurance, subrogation becomes even more important because limited settlement funds may have to cover medical bills, attorney fees, costs, and the injured person’s losses. Texas minimum auto liability coverage is only $30,000 per injured person, $60,000 per accident for bodily injury, and $25,000 for property damage, according to the Texas Department of Insurance.

When coverage is limited, the plan type and reimbursement rules can determine whether the injured person receives a meaningful net recovery. UM/UIM, PIP, MedPay, health insurance, multiple defendants, commercial coverage, rideshare coverage, and umbrella policies should be reviewed before accepting a limited offer.

For more on this issue, see Ryan Orsatti Law’s guide on what happens if the at-fault driver does not have enough insurance to cover medical bills.

How Long Do You Have to Resolve Subrogation in a Texas Injury Case?

Subrogation should be addressed before settlement funds are disbursed, and the injury lawsuit deadline should not be ignored while lien issues are pending. In Texas, a personal injury lawsuit is generally subject to a two-year limitations period under Texas Civil Practice & Remedies Code § 16.003, although special rules can apply to minors, government claims, wrongful death, and other situations.

Medicare can also affect timing. CMS explains that conditional payment information may be interim while the injury claim is pending, and the final conditional payment process has specific timing steps before settlement.

The practical point is simple: do not wait until the day checks are ready to begin lien work. Subrogation review should start while treatment and settlement evaluation are still underway.

How Does Ryan Orsatti Law Evaluate Subrogation in San Antonio Injury Claims?

Ryan Orsatti Law evaluates subrogation by identifying every payor, separating accident-related treatment from unrelated care, reviewing the governing plan or statute, and calculating the projected client net before settlement. In San Antonio and Bexar County injury claims, that often means checking private health insurance, Medicare, Medicaid, hospital liens, provider balances, PIP, MedPay, and UM/UIM issues together.

A typical review includes:

- Requesting lien and reimbursement ledgers.

- Auditing charges for unrelated care.

- Reviewing plan language and funding status.

- Checking for Texas Chapter 140 limits.

- Confirming Medicare or Medicaid recovery status when applicable.

- Searching for hospital lien filings when needed.

- Negotiating reductions when supported by the facts and rules.

- Preparing a settlement disbursement sheet before funds are released.

Ryan Orsatti Law helps injured people in San Antonio and across Texas evaluate fault, insurance coverage, medical bill issues, subrogation, and settlement net recovery before final decisions are made. To discuss a claim, you can contact Ryan Orsatti Law.

For government-benefit issues, see the firm’s guide on how Medicare and Medicaid affect a San Antonio personal injury settlement.

FAQs About Texas Health Insurance Subrogation

Do I have to pay back my health insurance from a Texas injury settlement?

You may have to pay back health insurance if the plan paid medical bills related to the injury claim and has valid reimbursement or subrogation rights. The amount depends on the plan language, whether Texas Chapter 140 applies, whether the plan is self-funded under ERISA, and whether the claimed charges are actually related to the accident.

Can health insurance take my whole personal injury settlement in Texas?

A health plan should not simply take the whole settlement without legal review. Texas Civil Practice & Remedies Code Chapter 140 limits many covered payor recoveries, but Medicare, Medicaid, ERISA plans, hospital liens, and other claims may follow separate rules. Before disbursement, the claimed amount should be audited against the settlement, plan documents, and accident-related medical charges.

What is the difference between subrogation and a medical lien?

Subrogation is usually a payor’s claim for reimbursement after it paid medical bills. A medical lien is usually a provider’s claim against settlement funds for unpaid treatment. In Texas, hospital liens are governed by Texas Property Code Chapter 55, while private health insurance subrogation may be governed by contract, Chapter 140, ERISA, or other law.

Does Medicare have to be repaid after a Texas personal injury settlement?

Medicare generally must be repaid for conditional payments it made for injury-related treatment when a settlement, judgment, award, or other payment is made. CMS uses a recovery process through the Benefits Coordination & Recovery Center and Medicare Secondary Payer Recovery Portal. The claimed charges should be reviewed because unrelated treatment can sometimes appear on a conditional payment list.

Does Texas Medicaid have a right to recover from my injury settlement?

Texas Medicaid may seek reimbursement when it paid for medical care related to an injury caused by a third party. Texas Medicaid third-party liability rules treat Medicaid as a payer of last resort, and recipients may have reporting duties when another person or insurer may be responsible. Medicaid recovery should be addressed before settlement funds are distributed.

Can a lawyer negotiate health insurance subrogation?

A Texas personal injury lawyer can often review, dispute, and negotiate health insurance subrogation claims, depending on the plan and facts. Common issues include unrelated charges, duplicate payments, excessive demands, Chapter 140 reductions, attorney-fee sharing, procurement costs, and whether the plan is fully insured or self-funded under ERISA. Not every claim can be reduced, but every claim should be verified.

Should I sign a settlement release before resolving health insurance subrogation?

You should know the likely lien and reimbursement picture before signing a settlement release. A release may end your claim against the at-fault party or insurer, but it does not automatically erase health insurance reimbursement claims, Medicare conditional payments, Medicaid recovery, hospital liens, or provider balances. A net settlement calculation should come before final approval.

What should I bring to a lawyer for a subrogation review?

Bring your health insurance card, EOBs, itemized medical bills, lien letters, Medicare or Medicaid notices, provider balance statements, settlement offer letters, police report, and any letters from recovery vendors. These documents help determine who paid, what was accident-related, what remains owed, and whether a reimbursement claim can be reduced or challenged.

Ryan Orsatti Law

4634 De Zavala Rd, San Antonio, TX 78249

Phone: 210-525-1200

ryanorsattilaw.com

This blog is for informational purposes only, not legal advice. Reading it does not create an attorney-client relationship. Past results do not guarantee future results.

Hurt in an accident in San Antonio? Learn how a San Antonio car accident lawyer can help with your claim. Call 210-525-1200 or request a free consultation. There is no fee unless we win.