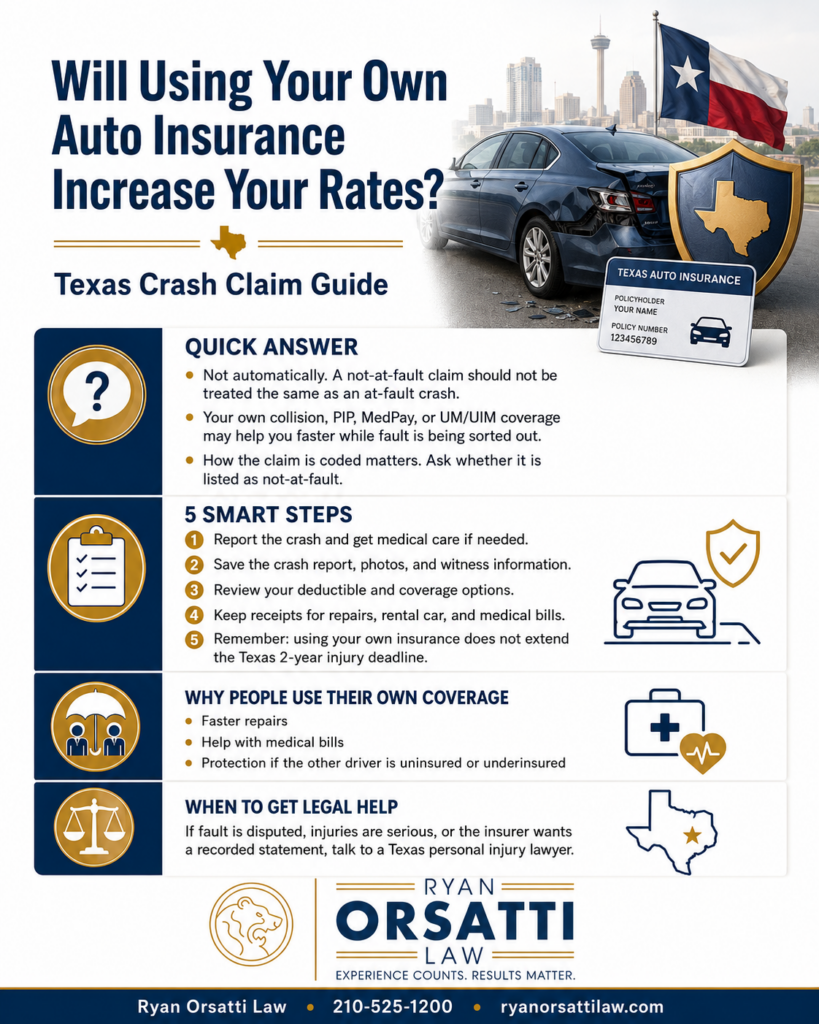

Quick Answer

Using your own auto insurance after a Texas crash does not automatically mean your rates will increase. The Texas Department of Insurance says auto insurers may consider accidents and claims history, and TDI’s glossary describes a surcharge as extra premium usually added for at-fault accidents, so a well-documented not-at-fault claim should not be treated the same way as an at-fault crash. (Texas Department of Insurance)

If the other driver delays, denies fault, has too little coverage, or leaves the scene, your own collision, PIP, MedPay, or UM/UIM coverage may protect you while fault and reimbursement are sorted out. Ryan Orsatti Law helps injured people in San Antonio and across Texas evaluate that choice before avoidable insurance mistakes are made.

Key Takeaways

- A not-at-fault claim should not be treated the same as an at-fault crash, but your claims history can still matter at renewal.

- Texas insurers may use CLUE reports to review claim history, so how the claim is coded matters.

- Using your own collision coverage may get your vehicle repaired faster, but you may have to pay your deductible first.

- PIP, MedPay, and UM/UIM can help when medical bills start before the at-fault insurer accepts responsibility.

- Filing with your own insurer does not extend the Texas injury lawsuit deadline.

- Before giving a recorded statement or signing a release, make sure you understand what claim you are making and what rights you may be affecting.

Will using my own auto insurance after a Texas crash increase my rates?

Using your own auto insurance might affect your premium, but it is not automatic, and a not-at-fault claim should be evaluated differently from an at-fault crash. TDI says auto companies may raise premiums based on accidents or tickets, and may use claim history, but TDI’s glossary describes a surcharge as extra premium usually added for at-fault accidents. (Texas Department of Insurance)

The practical issue is not just whether you file a claim. The issue is how the crash is documented, whether fault is disputed, what coverage you use, whether your insurer pays anything, and how the claim appears later in underwriting.

This matters in real Texas injury claims. TxDOT reported 14,905 serious injury crashes in Texas in 2024, causing 18,218 serious injuries, and 251,977 people were injured in motor vehicle crashes statewide. (TxDOT) For San Antonio drivers on Loop 1604, I-35, I-10, Loop 410, or US-281, waiting for the other carrier can mean delayed repairs, no rental car, unpaid medical bills, and pressure to make decisions before the evidence is complete.

What does Texas say about accident claims, rates, and surcharges?

Texas does not make every use of your own auto coverage a rate increase. TDI says premiums can go up depending on the type and number of claims, but companies cannot charge more for claims they did not pay, including denied claims, and cannot charge more just because you called to ask questions about your policy or the claim process. (Texas Department of Insurance)

TDI also explains that auto insurers use underwriting to decide whether to sell you a policy and what to charge, and that claim history may be reviewed through a CLUE report. (Texas Department of Insurance) That means a careful paper trail matters. Keep the crash report, photos, medical records, witness names, deductible receipts, and any letter showing the other driver accepted fault or reimbursed your insurer.

TDI’s auto guide also says an insurer generally cannot refuse to renew your policy because of accidents or incidents that cannot reasonably be blamed on you, unless you have more than one such claim in 12 months. (Texas Department of Insurance) That rule is not a guarantee that your premium will stay the same, but it is useful if an insurer treats one not-at-fault crash as a reason to drop you.

What is the difference between an at-fault claim and a not-at-fault claim in Texas?

The difference is whether the evidence shows you caused the crash or another driver did. Texas is a fault-based auto insurance state, meaning liability coverage generally pays for other people’s injuries and property damage when the covered driver is responsible for the crash. (Texas Department of Insurance)

Fault also matters because Texas uses proportionate responsibility. Comparative responsibility means Texas can reduce a person’s recovery by that person’s percentage of fault, and Texas Civil Practice and Remedies Code § 33.001 bars recovery if the claimant’s percentage of responsibility is greater than 50 percent. (Texas Statutes)

For rate concerns, the claim label matters. A crash coded as at-fault, chargeable, preventable, or disputed may create a different underwriting issue than a claim supported by a police report, photos, witness statements, and reimbursement from the other driver’s insurer.

Why does fault coding matter to your premium?

Fault coding matters because an insurer may later review the claim through internal records or a claim history report. TDI says companies may use CLUE reports to learn your claims history, and those reports can affect pricing or whether a company sells you a policy. (Texas Department of Insurance)

After a not-at-fault crash, ask your insurer how the claim is being coded. If the adjuster says the claim is listed as not-at-fault, ask for that in writing. If the insurer has bad or incomplete information, send the crash report, photos, witness information, repair documentation, and any letter from the at-fault carrier.

When should you use your own auto insurance instead of waiting on the other driver?

You should consider using your own coverage when the other driver’s insurance company is delaying, denying fault, claiming coverage is too low, or dealing with an uninsured, underinsured, or unknown driver. TDI says collision, UM/UIM, PIP, and MedPay may apply in different situations after a crash, depending on your policy. (Texas Department of Insurance)

The other driver’s insurer does not insure you. Your own insurer has a policy contract with you, which can make your coverage the faster path for repairs, medical-pay benefits, or uninsured motorist protection. The tradeoff is that you may have a deductible, claim-history concern, or reimbursement issue to track.

| Coverage you may use | What it may pay | Common rate concern | Practical note |

|---|---|---|---|

| Collision | Repair or replacement of your vehicle after a crash | It may appear in claim history, and you may pay a deductible first | Ask whether the claim is coded not-at-fault and keep deductible proof |

| PIP | Medical bills, lost wages, and certain accident-related expenses | It is a first-party claim, so ask how it affects discounts or renewal | TDI says Texas auto policies include PIP unless rejected in writing |

| MedPay | Medical bills after the crash | It may still appear in claim history | It is narrower than PIP because it focuses on medical bills |

| UM/UIM | Injury or property claims involving uninsured, underinsured, or hit-and-run drivers | It may require proof the other driver lacked enough coverage | Report hit-and-run crashes to police and preserve all fault evidence |

| Rental or towing | Rental car or towing costs if your policy includes it | Usually smaller than an injury claim, but still document it | Useful when the other carrier has not accepted responsibility |

Key takeaway: The right question is not simply whether to file with your own carrier; it is whether the benefit of faster repairs, medical-pay coverage, or UM/UIM protection outweighs the deductible and claim-history risk in your specific facts.

What should you do before filing with your own insurer?

Before filing, create a clean fault record and confirm which coverage you are using. TDI recommends getting the other driver’s information, collecting witness information, taking photos, telling your insurer as soon as possible, and sending the insurer records such as the police report and medical information. (Texas Department of Insurance)

Use this checklist after a Texas crash:

- Get medical care first if anyone may be injured.

- Call police if anyone is hurt, the crash is serious, or the other driver fled.

- Photograph the vehicles, license plates, road conditions, signals, debris, skid marks, and visible injuries.

- Exchange driver, insurance, and contact information.

- Save witness names, phone numbers, and short statements if they are willing.

- Ask for the crash report number and request the TxDOT CR-3 when available.

- Review your declarations page for collision, rental, PIP, MedPay, UM/UIM, and deductibles.

- Notify your insurer with facts, not guesses about fault or long-term injuries.

- Ask the adjuster to confirm in writing how the claim is being coded.

- Keep deductible receipts, rental receipts, repair estimates, medical bills, and all insurer letters.

- If you were injured, speak with a Texas personal injury lawyer before signing broad releases or giving statements that go beyond basic facts.

Ryan Orsatti Law’s San Antonio car accident lawyer resource explains how injury claims are evaluated after local crashes. If medical bills are already arriving, the firm’s guide on who pays medical bills after a car accident may also help you understand the coverage issues.

What if your premium goes up after a not-at-fault claim?

If your premium goes up after a not-at-fault claim, ask your insurer for the written reason and compare it to the claim file, crash report, and evidence of fault. TDI recommends first talking to the company, sending supporting documents, and then filing a complaint if the issue is not resolved with a regulated insurer. (Texas Department of Insurance)

A premium change may be caused by several things. It may be tied to the crash, a general rate change, a lost discount, a vehicle change, your ZIP code, your household driver history, or a claim-history report. Do not assume the reason. Ask for the specific explanation.

You can also request your CLUE report. TDI says you may get a free copy of your CLUE report each year, and that report can show claim history used by insurers. (Texas Department of Insurance) If the claim is wrong, incomplete, or coded as at-fault without support, ask the insurer and reporting company how to dispute or correct it.

How does using your own insurance affect your injury claim?

Using your own insurance can help with repairs or early bills, but it does not end your injury claim against the at-fault driver unless you sign a release. The bigger injury-claim issues are subrogation, deductible reimbursement, medical-bill documentation, lien handling, and avoiding inconsistent statements.

Subrogation means an insurer may have the right to pursue reimbursement from another insurer or legally responsible party after it pays benefits. TDI’s glossary defines subrogation as the right of an insurance company to seek payment from another insurer or person after paying a claim. (Texas Department of Insurance)

That is why using your own coverage is not just an insurance-rate decision. It can affect the accounting of the claim. If collision pays property damage, PIP pays medical bills, health insurance pays treatment, or UM/UIM becomes involved, the settlement paperwork must account for those payments correctly.

For related claim issues, see Ryan Orsatti Law’s guides on the insurance adjuster phone call, vehicle repair cost limits, and the San Antonio car accident settlement timeline.

Can your insurer get reimbursed from the at-fault driver?

Yes, your insurer may try to recover what it paid from the at-fault driver’s insurer. TDI says if your insurer recovers money from the other driver’s insurance company, your insurer must try to recover your deductible too, and the deductible may be reimbursed depending on the recovery. (Texas Department of Insurance)

This process is one reason collision coverage can be useful after a not-at-fault crash. You may get repairs moving before the other carrier finishes its liability review. The risk is that you need to track the deductible and make sure the claim is documented as not-at-fault if the evidence supports that position.

Can an insurance statement hurt your injury claim?

Yes, an insurance statement can hurt an injury claim if it is incomplete, speculative, or inconsistent with medical records. You may have duties to cooperate with your own insurer, but you should not guess about speed, distance, fault, prior injuries, future treatment, or whether you are “fine” when symptoms are still developing.

This is especially important in soft-tissue, concussion, spinal, and delayed-treatment claims. A short recorded statement can become a claim exhibit later. Keep statements factual: where the crash happened, what direction vehicles were traveling, what you observed, what hurts, and what medical care you have received so far.

Attorney Insight: In a San Antonio not-at-fault crash, the rate issue often turns on how the claim is documented before renewal. Adjusters may not control underwriting, but their liability notes, photos, witness statements, crash report, and subrogation outcome can affect how the claim appears later. Fixing a bad fault label early is usually easier than cleaning it up months later.

How long do you have if using your own insurance does not solve the injury claim?

Using your own insurance does not extend the deadline to file a Texas personal injury lawsuit. Texas Civil Practice and Remedies Code § 16.003 generally gives an injured person two years to file suit for personal injury, and missing that deadline can create a serious legal problem. (Justia)

Insurance negotiations can take months, especially if treatment is ongoing, liability is disputed, or UM/UIM coverage is involved. A claim can feel active because adjusters are calling, bills are being reviewed, or repairs are pending. That does not mean the lawsuit deadline stopped.

If settlement discussions fail, the legal question becomes whether suit must be filed. Ryan Orsatti Law’s guide on whether you can sue after a car accident explains the difference between an insurance claim and a lawsuit.

When should you call Ryan Orsatti Law before using your own insurance?

You should consider calling Ryan Orsatti Law before using your own coverage if you were injured, fault is disputed, the other driver was uninsured or underinsured, the insurer wants a recorded statement, or your bills already exceed available coverage. These are the situations where a quick insurance decision can affect fault, medical documentation, reimbursement, and deadlines.

Ryan Orsatti Law helps injured people in San Antonio, Bexar County, and across Texas evaluate fault, collision coverage, PIP, MedPay, UM/UIM, deductibles, subrogation, medical bills, and claim timing. The goal is to make an informed decision before the insurer’s paperwork, claim coding, or statements create avoidable problems.

A lawyer is not needed for every minor property-damage claim. But if there are injuries, missed work, disputed fault, a hit-and-run, low policy limits, a commercial vehicle, a rideshare driver, or a serious medical diagnosis, the insurance choice should be reviewed in the context of the whole claim.

Frequently Asked Questions

Will my insurance go up if I was not at fault in a Texas crash?

A not-at-fault crash does not automatically mean your Texas auto insurance premium will increase. TDI says premiums may depend on the type and number of claims, and TDI’s glossary describes a surcharge as extra premium usually added for at-fault accidents. Ask your insurer how the claim is coded and keep proof that another driver caused the crash. (Texas Department of Insurance)

Should I tell my insurance company about a crash if I plan to use the other driver’s insurance?

Yes, you should usually notify your own insurer after a crash, even if you expect the other driver’s insurance to pay. TDI recommends letting your insurer know and getting the police report if police investigated. Keep the report factual, avoid guessing about injuries or fault, and review your policy deadlines for notice, PIP, MedPay, collision, or UM/UIM coverage. (Texas Department of Insurance)

Will a collision claim raise my Texas auto insurance rate?

A collision claim can affect claim history, but that does not mean every collision claim causes a rate increase. If another driver caused the crash, your insurer may pursue reimbursement from the at-fault driver’s carrier, and your deductible may be recovered if that effort succeeds. Ask the adjuster to confirm whether the claim is coded as not-at-fault. (Texas Department of Insurance)

Does using PIP or MedPay mean I caused the crash?

No. Using PIP or MedPay does not mean you caused the crash. These are first-party benefits under your own auto policy. TDI says PIP pays medical bills, lost wages, and certain accident-related expenses, while MedPay pays medical bills. PIP is included in Texas auto policies unless rejected in writing. (Texas Department of Insurance)

Can my insurer nonrenew me after one not-at-fault accident in Texas?

TDI says an insurer generally cannot refuse to renew your policy because of accidents or claims that cannot reasonably be blamed on you, unless you have more than one such claim in 12 months. That does not guarantee your rate will stay unchanged. If renewal changes after a not-at-fault crash, ask for the written reason. (Texas Department of Insurance)

What should I do if a Texas insurer says the crash was partly my fault?

Ask for the insurer’s written explanation and the evidence supporting any fault percentage. In Texas, fault matters because Civil Practice and Remedies Code § 33.001 bars recovery if a claimant is more than 50 percent responsible. Preserve the crash report, photos, witness information, repair data, medical records, and any statement that supports your version of events. (Texas Statutes)

Can filing with my own insurance hurt my personal injury case?

Filing with your own insurer can hurt your injury claim if you give inconsistent statements, sign a broad release, fail to document medical care, or miss the lawsuit deadline. The filing itself does not usually settle your bodily-injury claim against the at-fault driver. If injuries are significant or fault is disputed, get advice before making recorded statements or signing claim documents.

Ryan Orsatti Law

4634 De Zavala Rd, San Antonio, TX 78249

Phone: 210-525-1200

ryanorsattilaw.com

This blog is for informational purposes only, not legal advice. Reading it does not create an attorney-client relationship. Past results do not guarantee future results.

Hurt in an accident in San Antonio? Learn how a San Antonio car accident lawyer can help with your claim. Call 210-525-1200 or request a free consultation. There is no fee unless we win.